When Harry Met Rally…

Harry Browne’s Classic Portfolio, Reimagined with Momentum

Harry Browne’s Permanent Portfolio is about as simple as it gets: equal weights in stocks, gold, bonds, and cash. It’s been around forever. But does this old-school approach still hold up?

The Original Flavor

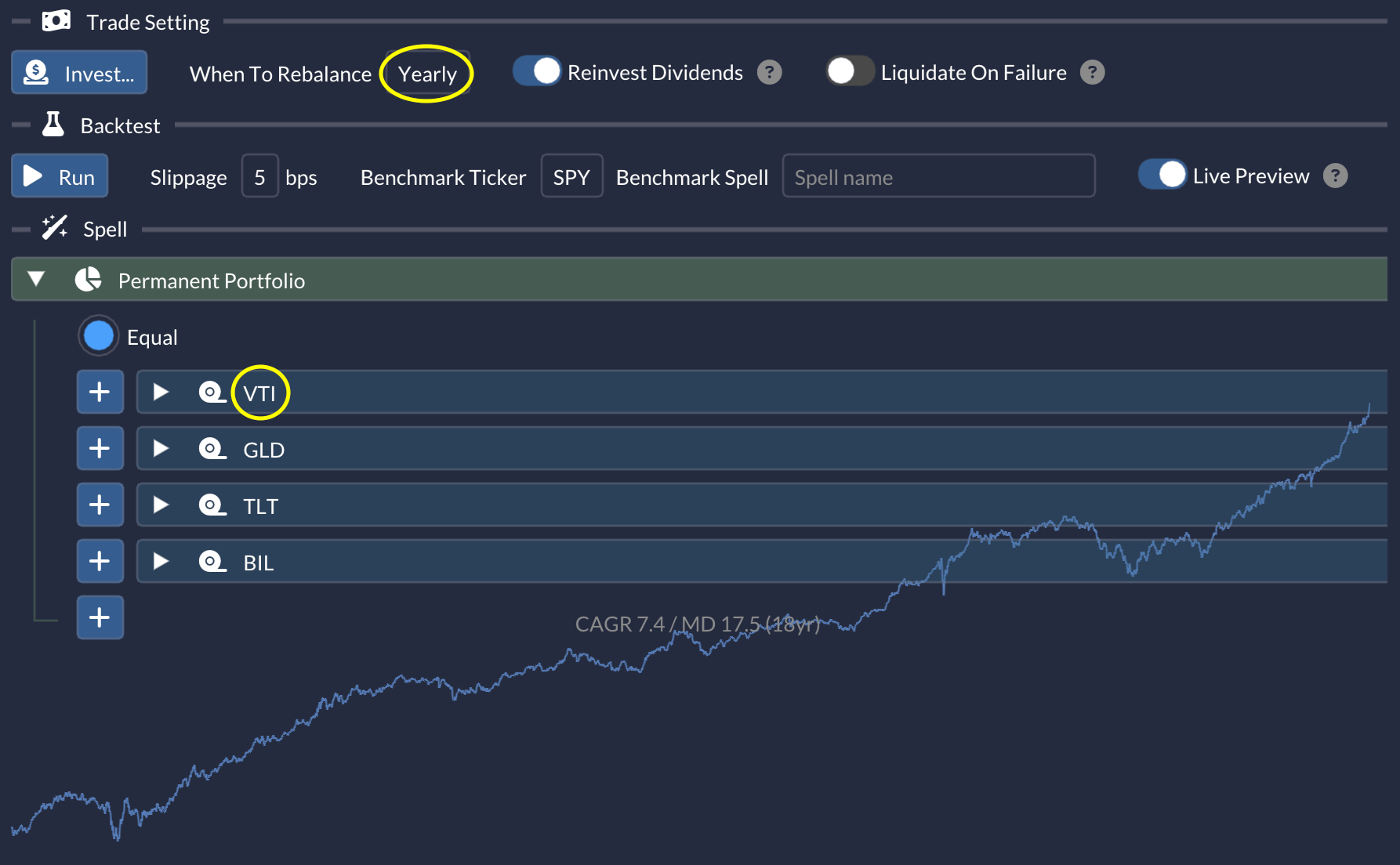

As you can see, implementation in QuantMage is dead simple. I used annual rebalancing with VTI for stocks. Over the last 18 years, it delivered an annual return of 7.4%. Not exactly a “print money” headline—but the surprising part is the quality of the ride: a Sharpe of 1.02 from such a basic allocation is nothing to ignore.

⚠️ Just a heads-up: None of this is financial advice. Just one mage tinkering with spells. Always DYOR and consult a qualified advisor if needed.

Jazzing It Up

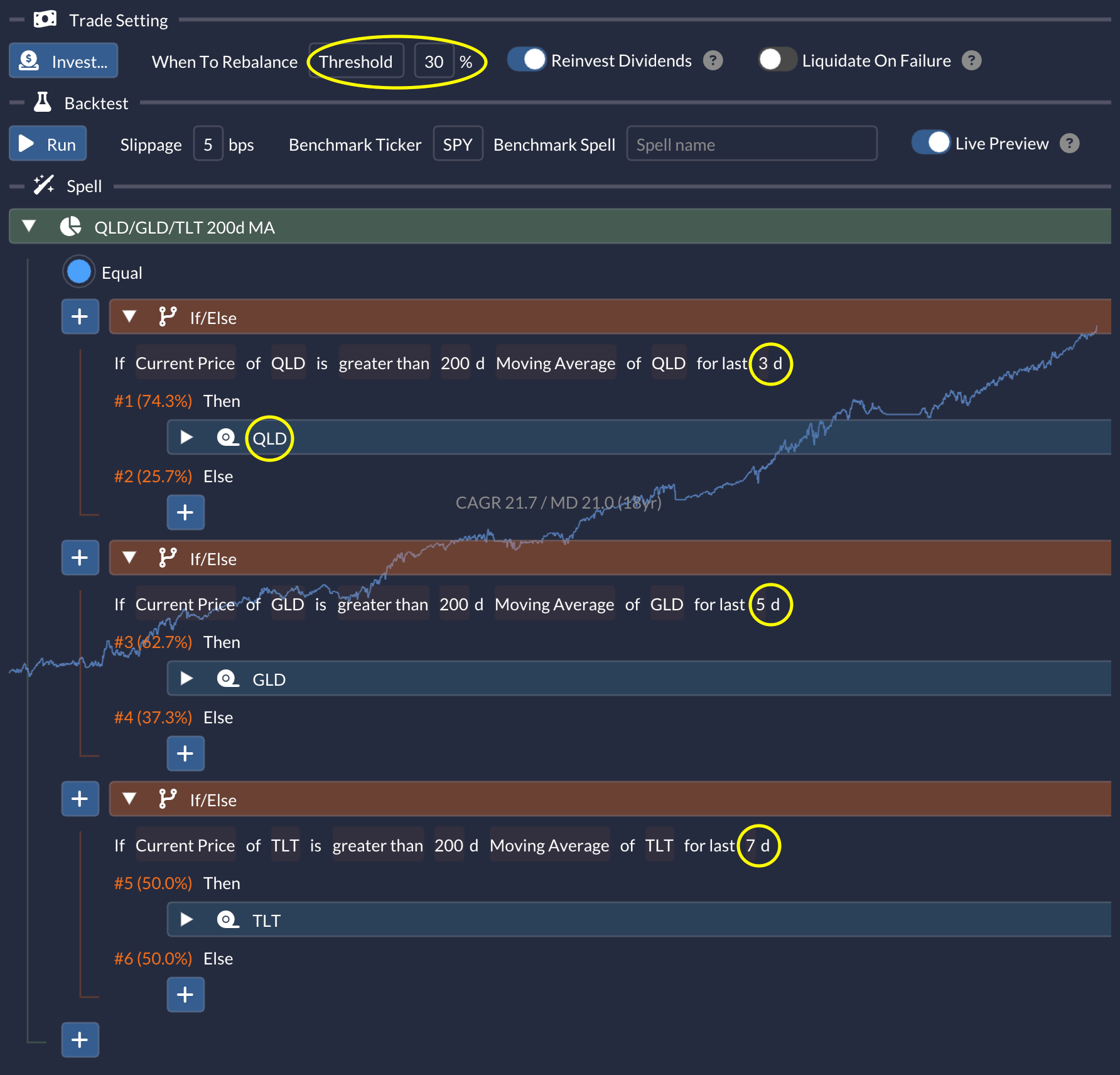

For those who want more action, we can add a momentum filter and ditch the cash. Each asset gets checked against its 200-day simple moving average—only those with confirmed breakouts make the cut. This takes advantage of how QuantMage handles empty branches under equal weighting. I also swapped in QLD (2x leveraged QQQ) for extra juice, and tweaked the momentum check durations across asset classes to polish the historical results. Fair warning: more tuning means more overfitting risk. Also a threshold rebalancing is used this time.

The simulated results? A 21.7% CAGR over 18 years. Hitting that kind of return while keeping volatility in check (Sharpe and MAR both above 1.0) is no small feat:

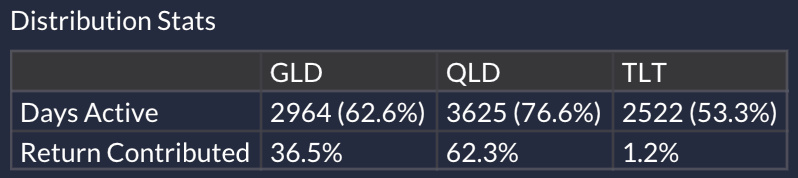

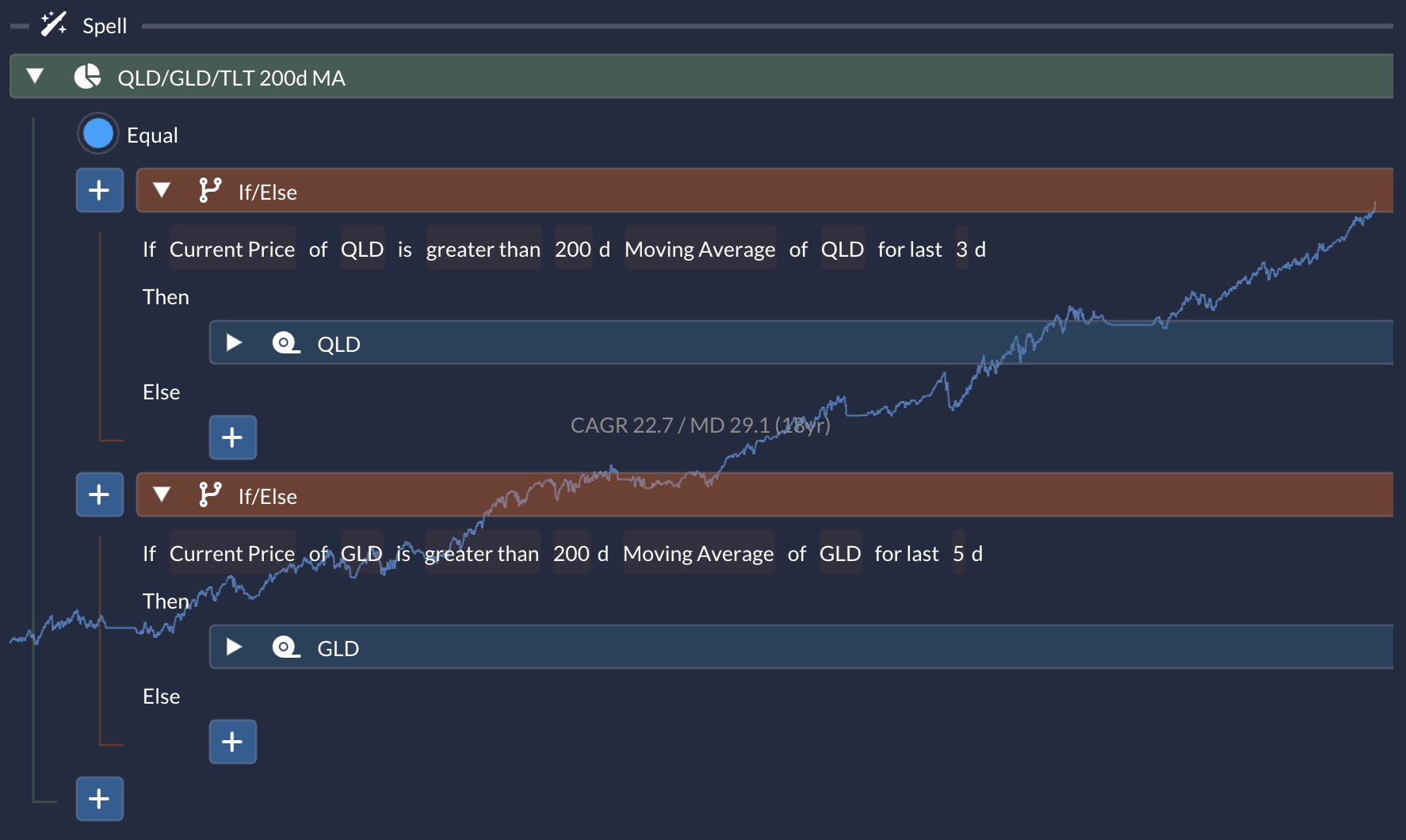

Digging into the stats, you might think TLT (bonds) is slacking—just a 1.2% return while active more than half the time. But its real job? Playing defense. Take it out, and the portfolio’s risk-adjusted return noticeably suffers:

Final Thoughts

This little experiment is a nice reminder that you can get a surprisingly decent risk-adjusted return with a portfolio that fits on a sticky note—just three or four ETFs.

No, it’s not invincible. A year like 2022 can still hurt—when stocks and bonds struggle and gold doesn’t bail you out cleanly, both versions can take a hit. But over nearly two decades, the overall track record is still… not something I’d sneeze at.

Curious what you think:

Are momentum filters here “signal” or mostly “curve-fit glitter”?

Does TLT-as-crash-padding still make sense in a world where bonds can have equity-like drawdowns?

Would you rather keep cash (protection) or replace it with “sit out when trend is down” (optionality)?

Big shoutout to Martin for sparking this idea with his recent article.

Great stuff, JJ. This is exactly what I hope for when I publish an idea -- that somebody improves on it. Excellent work done, and for no charge, to boot!

Thanks a ton for mentioning me, but I'm just a guy standing on the shoulder of a giant, as it were. Harry Browne has shown that you can achieve reasonable returns, with a MAR of not much less than 1, with around 15 minutes of work per year. (Just by re-balancing stocks, treasuries, gold and cash). And that this has worked literally for decades.

Diving deeper into the subject, one discovers that over the years, there have been numerous attempts to improve on the original Harry Browne scheme. And none have really worked out all that well, except for yours (looking forward too, I hope) and mine (perhaps). Most got destroyed in 2008 and 2022.

What I'd like to do is add an international scope to HB. (You know I'm a sceptic about the $SPX mid-term...) ACWI with international bonds, gold, and cash, preferably in a currency mix. This may be above my pay grade, but no harm in trying!